The shift to a tokenized economy begins with digital assets. The blockchain provides the ledger to record their ownership and cryptographically secure it from tampering. It is sophisticated to use at the moment, and not as easy to understand. There are still many people who don’t have an understanding of cryptocurrency and even what the blockchain can do. They are just beginning to become aware of their benefits. Plenty of hand-holding is required to get more on board to put their trust in a new financial system.

According to research by the Bank of New York Mellon:

“There is an increasing demand in the market for a traditional, established custodian to provide secure storage of cryptocurrencies.”

Many are probably not aware they are already using a form of custody solution. A perfect example is digital exchanges like Binance and Coinbase. Users who have not moved their digital assets from these exchanges are entrusting them in custodial wallets. The users do not possess their private keys and the exchange provides a way to manage these assets on the blockchain. Most newcomers to the cryptocurrency scene are probably better off this way in the beginning because of their lack of knowledge. Then there are users who would prefer the traditional third party to help them manage their digital assets like a typical investment portfolio.

Digital Asset Custodians (DAC)

This is where Digital Asset Custodians (DAC) come into the picture. They offer their services much like traditional finance institutions to customers who need their assistance. This is actually a good onboarding route for first-time digital asset investors. The DAC can handle the service as a trusted third party who will be responsible for maintaining and managing the customer’s digital assets. In the real world, there are still many people who prefer this type of relationship as opposed to a totally independent non-third party solution.

Digital Asset Custodians aim to deliver financial services on the blockchain, using a trusted system of smart contracts, for digital assets like pension funds and tokens. This provides customers with a third party provider to secure their digital assets. These forms of custody solutions are the norm many people have become accustomed to with regards to financial services. In the cryptocurrency space, this is not exactly the model for decentralization but puts the responsibility in the hands of others. If that can bring peace of mind then there will be a great use case for it.

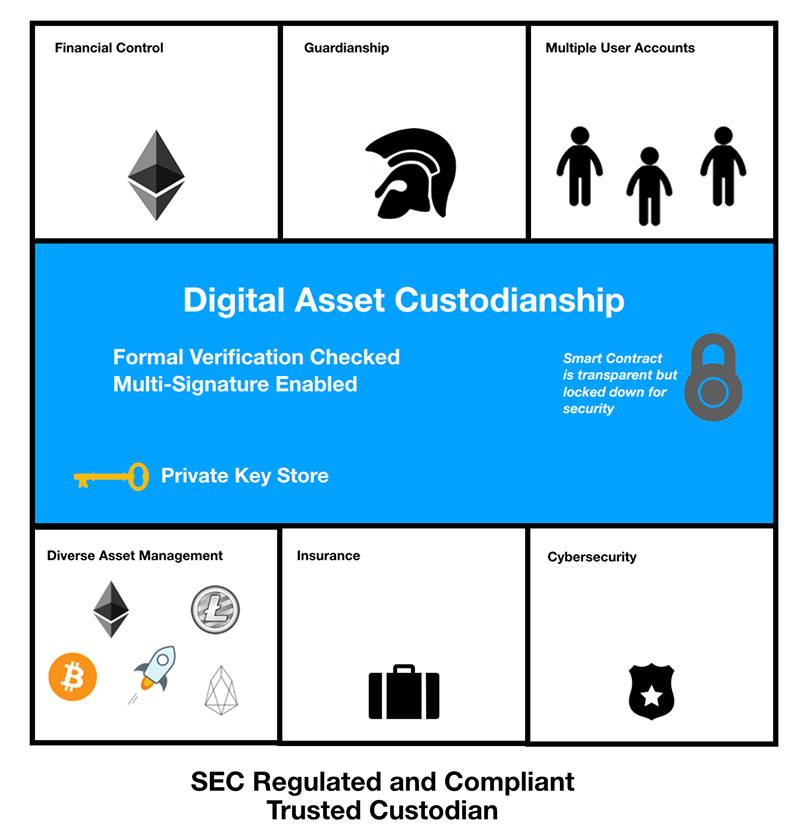

The DAC can implement what is called a smart contract that provides the custodianship of digital assets stored on the Ethereum network, or another blockchain platform. The DAC uses API (Application Programming Interface) that interacts with both on-chain and off-chain services using a micro-service architecture approach with the following functions:

- Financial controls (multiple signers, audit trails, etc.)

- A regulated digital asset guardian

- Multi-user accounts with separate permissions

- Support for a wide range of digital assets and currencies

- Insurance (in some cases)

- Cyber and physical security

The responsibility is heavy on the DAC. They have to treat the digital asset as if it were their own. They will also be regulated by the government to comply with laws regarding cryptocurrency.

Demographics Of Traditional Investors

Some traditional investors don’t have an understanding of how cryptocurrency works. Unlike traditional investing, where you look at an index and collect dividends, cryptocurrency works in a different way. The on-boarding process is also much more difficult since the demographics also tend to be in a different age range. Millennials, who are more tech-savvy, grew up on the Internet from an early age. They can quickly learn how to set up a digital wallet and trade on a digital exchange.

According to Fortune, when it comes to cryptocurrency like Bitcoin:

“An overwhelming 71 percent of them are male. The majority — 58 percent — are young, between the ages of 18 and 34 years old. And unlike the broader U.S. population, nearly half of them are minorities.”

Whereas the 50 and up to age range who are the potential investors into cryptocurrency is not yet getting into cryptocurrency. It is a steeper learning curve for some, while for others it is either because they don’t often use computers or have not yet heard of cryptocurrencies like Bitcoin or Ethereum.

When you have financial institutions ready to offer these services, onboarding becomes an easier task. Custodial services are being offered by the likes of Fidelity Investments and other companies are following. Banks are also ideal for being a DAC because they already have customers willing to use their service. The DAC, in this case, will teach traditional investors how to put money into cryptocurrency using different types of financial instruments which are regulated and approved by the government. That way investors are guaranteed that what they are doing is totally legal. That gives more confidence for an investor who usually trades stocks to get into a more volatile market like cryptocurrency.

Despite the volatility, DAC will most likely provide their customers with a smart contract that lock digital assets. In this case, the DAC will handle all aspects of trading, much like the way a stockbroker works. When the price value is high, they can sell off some of the cryptocurrency and then buy back at lower price levels. Most likely the digital assets will be liquidated into a stable coin during times of great volatility to minimize any losses. Other customers may simply HODL (Hold On For Dear Life), especially if they are treating it as a long term investment and store of value.

Cons Against DAC

There are of course cons against having a third party handle digital assets. The cryptocurrency was made to be P2P (Peer-to-Peer) and totally independent from third party or arbitration during a transaction. There are even DEX (Decentralized Exchanges) which are autonomous to a certain extent, functioning as a platform but never possesses or holds a user’s digital assets during a transaction. No one is in control of your money but yourself. Yet there are still investors who don’t really care about decentralization, but more about their portfolio management. They entrust the care of their digital assets into the hands of the DAC.

In terms of security, this may not be the most secure since a hack into the custodian’s systems can affect customers severely. Investors are probably aware of the risk, but they would rather trust an expert than to try to do it on their own. Some of these investors also do not have time to check the market and actively trade, especially among retirees and pensioners who just want to relax.

Potential Markets

The market looks very big for financial services in cryptocurrency trading and investments. Tapping into traditional markets like pensions, insurance and futures are generating plenty of excitement in the cryptocurrency market. What these markets will bring is much-needed liquidity that will pump prices. the following lists the amount of money the following market are worth.

Potential Markets And Their Value (US Dollar)

- Pensions ($41.3 Trillion Global) (Source)

- Insurance ($1.2 Trillion in the US) (Source)

- Futures Contracts ($12.7 Trillion — $542 Trillion) (Source)

If a certain percentage were to enter the cryptocurrency market, thru on-boarding via a DAC, that can bring in billions to trillions into the market cap. As of May 2019, the total cryptocurrency market cap has never gone over $1T so liquidity will play a role in getting there. Once there is liquidity, there will be price stability and less volatility. How DAC can help is bringing in more money by volume of transactions. Higher trading volume is what brings in more liquidity and that affects the price value of digital assets positively.

Let’s say for example 25% of global pension funds (P) enter the cryptocurrency market. That would be:

P = 0.25(41.3 Trillion) = 10.325 Trillion

If the total market cap (M) were at $192 Billion then:

Total Market Cap = M + P = 10.517 Trillion

That is a considerable amount of liquidity. Now it can further increase as more people are on-boarded and there is a network effect. Depending on the rate of acceptance among the market, if demand increases so will the total market cap as more money enters the market.

Regulation

Now that traditional financial institutions are offering instruments to digital assets, regulation will play a big role. In the US, customers will be required to keep client funds with a qualified custodian. However, cryptocurrency is a new type of asset class that really does not have well-defined rules or clarity. The regulation provides customers who invest money with these custodians protection from fraud and misappropriation of digital assets. This is the type of law traditional investors need, knowing that their custodian will be liable in such cases.

Whether it is testing the waters or becoming the norm, traditional investing methods into cryptocurrency helps bring in liquidity. Never mind that these investors don’t control their own digital assets. They need a DAC to help them, and this is how some if not many will get into the market. With more clarity in regulation, custody solutions can become more mainstream as the ideal entry point for cryptocurrency investing.

It is also not just traditional investors in retail that DAC offers their services to. It will also be a path for bigger institutional investors to enter the market, thanks to regulations clarity to digital asset trading and ownership. The trust that these establishments need is offered by the DAC to provide them the management and security services they need for their digital assets. The lack of services that offer to help investors in the cryptocurrency market has long been considered a roadblock. What was once a roadblock now has a path to the blockchain and this can surely open up space to more interest.

Try to figure out the solution of the Rubik’s Cube with the online simulator. See how far you can get.